Variance and covariance of a weighted portfolio

You should not be reading this post; shoo, get a life.

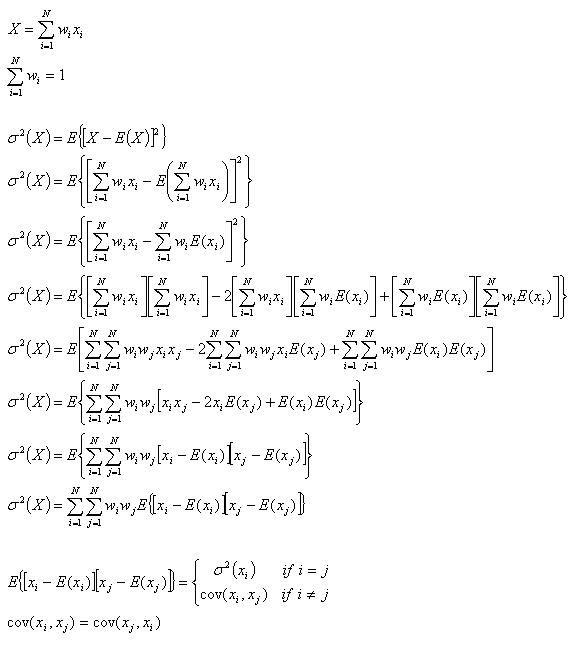

Was fiddling with some equations on my flight from Shanghai and Tianjin, and the following came about. The stuff I found in the text was unsatisfactorily complicated and not generalised enough.

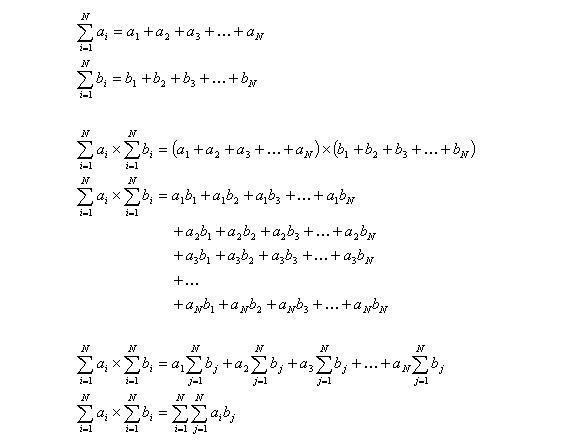

I think the most conceptually challenging part of the preceding definition of variance lies in the sudden appearance of the index j (this appears on line 5). A brief illustration follows, showing how the additional index is summoned:

Was fiddling with some equations on my flight from Shanghai and Tianjin, and the following came about. The stuff I found in the text was unsatisfactorily complicated and not generalised enough.

I think the most conceptually challenging part of the preceding definition of variance lies in the sudden appearance of the index j (this appears on line 5). A brief illustration follows, showing how the additional index is summoned:

Labels: finance, mathematics

posted by Tan Yee Wei at 4/04/2008 10:09:00 am

![]()

![]()

<< Home